In September, the Consumer Financial Protection Bureau (CFPB) issued its final ruling on an amendment to Regulation B of the Home Mortgage Disclosure Act (HMDA). It also noted its intent to assist with compliance with Regulation C. The amendment, which follows a 2015 congressional update, will go into effect starting January 1, 2018. Ultimately, it is designed to give creditors more flexibility to meet standard government regulations, but banks are generally unprepared for the changes, in part because the standards have been moving targets.

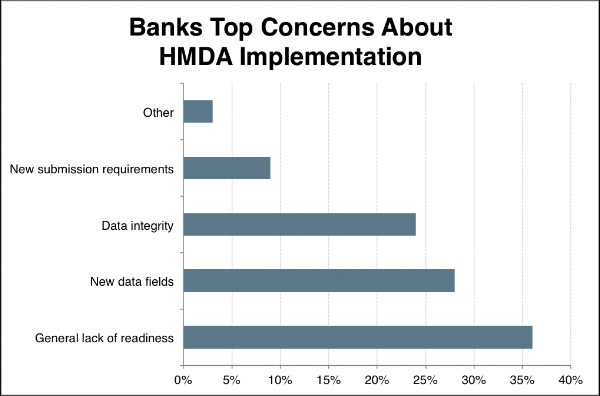

Global information services company Wolters Kluwer recently polled nearly 700 banks about their readiness for the new requirements. They learned that 76% of banks said they still lacked a process to collect and report on the 110 data fields required under HMDA in 2018. In large part, the lack of preparedness is because HMDA decisions have continued to shift. [1]

Global information services company Wolters Kluwer recently polled nearly 700 banks about their readiness for the new requirements. They learned that 76% of banks said they still lacked a process to collect and report on the 110 data fields required under HMDA in 2018. In large part, the lack of preparedness is because HMDA decisions have continued to shift. [1]

In particular, the CFPB continues to institute and issue changes related to compliance – like the only recently published Planned Small Entity Compliance Guide.[2] The lack of stability has challenged banks to ready themselves for the implantation deadlines. Adding to the challenge, the CFPB’s HMDA platform, through which LAR (loan application register) data should be reported is not yet ‘turned on’ to allow banks and vendors to submit their expanded data set.

Changes to HMDA

In 1975, Congress passed the Home Mortgage Disclosure Act (HMDA) to help meet three primary objectives: “[serve] housing needs…attract private investment to areas where it is needed… [and identify] possible discriminatory lending patterns.”[3] (FFIEC, 2017) The act originally was monitored by the Federal Reserve. In 2011, the Consumer Financial Protection Bureau (CFPB) took over enforcement.

In 2015, Congress passed an update to HMDA, which will go into effect January 1, 2018. The update brings extensive changes including reporting on 48 data fields, adding 25 new data fields to the current 23, and modifying 20 of the existing fields. [4] Regulation B creditors making mortgage loans are subject to collect applicant information using either the aggregate ethnicity and race categories, or disaggregated ethnicity and race categories and subcategories, as outlined in the Regulation C appendix, as amended by the 2015 and 2017 HMDA Final Rules. The final rule also makes changes to the appendix of Regulation B, which provide two alternative forms to collect applicant ethnicity, race, and sex information. Effective January 1, 2022, the rule removes an outdated version of the URLA (Universal Residential Loan Application).

Financial institutions will collect HMDA data around a variety of factors, including:

- Age

- Originator

- NMLS identification

- Credit score

- Combined loan-to-value (CLTV) ratio

- Borrower's debt-to-income (DTI) ratio

- Borrower-paid origination charges

- Points and fees

- Discount points

- Lender credits

- Loan term

- Prepayment penalties

- Interest rates

All changes include a model form and cross-reference for collecting aggregate applicant race, ethnicity, and sex information. The CFPB notes that, as published, the summary provides guidelines only. It is not a substitute for the final ruling, which gives Regulation B creditors flexibility in collecting the applicant information.

Preparing for HMDA Data Collection Changes

As HMDA goes into effect in 2018, financial institutions will have to more than double their current data collection efforts. Despite the uncertainties and the volume of changes, you need to be prepared to report the new data by 2019.

No doubt, financial institutions need to ensure they are updating their applications appropriately, starting now. HORNE is committed to educating clients about the pending implementation requirements to make sure that they are prepared for this massive change. We are considering known and expected outcomes, including looming privacy issues and the legal ramifications that might arise as the CFPB balanced collecting data for the common good and the perception of privacy invasion.

If your bank is just getting started or if you have questions about how to navigate the changes, please contact your HORNE Banking advisor.

Join the conversation and receive updates of new posts:

[1] http://www.bankingexchange.com/compliance/fair-lending/item/7107-hmda-processing-readiness-lags

[2] https://s3.amazonaws.com/files.consumerfinance.gov/f/documents/201710_cfpb_KBYO-Small-Entity-Compliance-Guide_v5.pdf

[3] Background & Purpose, Federal Institutions Examination Council, FFIEC, 2017

[4] The new Home Mortgage Disclosure Act (HMDA) Rule, Mortgage Bankers Association MBA, 2017

Leave A Comment